yahoo Press

Global light vehicle market falters in February

Images

1 / 5

2 / 5

3 / 5

4 / 5

5 / 5

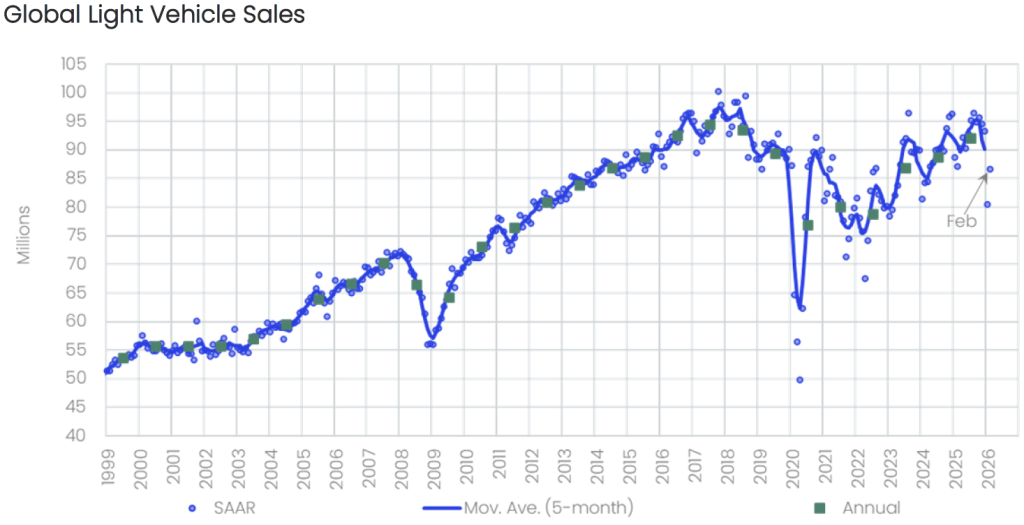

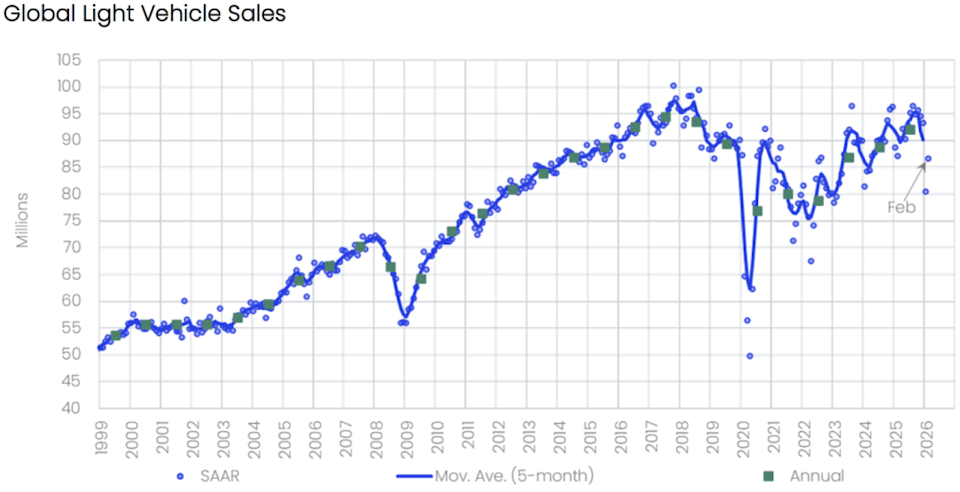

For February, the Global Light Vehicle (LV) selling rate improved modestly to 86.6 mn units/year, on what was a weak start to 2026. In year-on-year (YoY) terms, the market declined 8.5% YoY due to a second consecutive sharp contraction in the Chinese passenger vehicle (PV) market as sales totaled 6.0 mn units globally. Global LV sales showed signs of faltering last month as both China and US saw a notable decline in sales. China’s steep contraction remains a key drag on global sales volumes as consumers feel the effects of less policy support, while in the US, weak EV sales and affordability concerns are weighing on LV demand. Western Europe’s February total was promising as sales rebounded from a weak January figure. Looking ahead, the recent developments in the Middle East and the ensuing shock to energy prices and supply chains present the global LV market with serious headwinds to sales this year, keeping the outlook tilted to the downside in the near term. North America US Light Vehicle sales fell by 3.6% YoY in February, to 1.18 mn units. The month contained the same number of selling days as February 2025, enabling a direct comparison. The annualized selling rate accelerated to 15.6 mn units/year in February, from 14.7 mn units/year in January. The market continued to be held back by weak EV sales, while affordability remains a concern. For a second consecutive month, winter weather may have had an impact, with a snowstorm in the Northeast the culprit in February. Average transaction prices reached US$45,876 in February, down by US$327 MoM, but up by 1.8% YoY. Canadian Light Vehicle sales totaled an estimated 119k units in February, down by 0.4% YoY, while the selling rate slowed to 1.95 mn units/year, from 2.01 mn units/year in January. As has typically been the case in recent months, the market performed reasonably well, considering poor weather and a difficult economic and trade environment. In Mexico, sales increased by 2.7% YoY, to 127k units. The selling rate eased to 1.71 mn units/year, from 1.74 mn units/year in January, but the market continues to outperform its regional peers as it becomes more diverse. Europe The Western European LV market saw a modest improvement in February as sales totaled 986k units, up 1.6% YoY. The monthly selling rate also improved, accelerating to 14.6 mn units/year. YTD sales currently stand at 2.27 mn units, down 2.3% from the same period in 2025. Results across much of Western Europe were positive, although a sharp contraction in France acted as a significant headwind and weighed on overall regional growth. In light of recent developments in Iran, which has disrupted energy markets and could intensify inflationary pressures across the region, we have taken a slightly more cautious outlook for the 2026 Western European PV forecast, expecting sales to remain broadly flat this year. In Eastern Europe, the LV selling rate slowed to 4.75 units/year. Russia’s LV market remained weak in February 2026, with sales declining 5.7% YoY to around 74k units, though volumes rose 2.0% MoM from January’s unusually low base. Demand remains subdued after a VAT hike and a 10-20% increase to the vehicle recycling fee at the start of the year. The Turkish PV market fell for the first time in a year as sales totaled 70k units down 8.2% YoY. After a record-breaking 2025 where sales exceeded 1 mn units, the Turkish PV market is seeing signs of a potential stabilization in sales. China China’s PV sales sank 32.5% YoY to 975k units in February, the lowest PV topline since April 2022, and the third lowest since 2018. YTD, this leaves the opening two months of PV sales down 24.9% YoY. On a selling rate basis, things looked brighter from a monthly perspective, with the metric improving 28.9% MoM to 17.7 mn units/year, though the rate fell 6.3% YoY. Sales in China are facing significantly less policy support in the short term as the NEV tax discounting was reduced at the end of last year, and regionally varied lags in the updated trade-in subsidy scheme’s implementation leave consumers with little reason to rush to buy. We expect the implementation to be integrated into most provinces by the beginning of March. We remain unchanged on our LV topline this month as we see the full implementation of the updated trade-in subsidy (as of late February) sparking some momentum and easing pull forward retraction as the year progresses (last year's pull forward effect from the NEV change pulled demand from 2026 sales). But there are notable downside risks to the outlook, mainly if the Middle East disruption extends beyond four to six months. Looking further ahead, we see weakness in the market in 2027 and 2028 as the expectations on subsidy support ending in 2026, NEV tax discounting continues to fall off, and prices return to normal. Other Asia In Japan, LV sales fell by 3.8% YoY to 390k units in February. The PV market led the weakness with a 6.8% contraction. This leaves the market down 3.2% YoY for 2026 YTD as January shrank by a lesser 2.5%. However, when looking at the average selling rates for this year, the picture worsens with a 4.2% decline. The persistent weakness in Japan has been driven by a weak economic backdrop as well as rising financing costs as the policy rate has risen to a decades-high in recent months. Korean LV sales fell 6.2% YoY in February after expanding 15.4% in January, with the first month of the year benefitting from an extra working day due to the calendar of the 2026 Lunar New Year holidays. However, February’s raw data retraction is reframed in selling rate terms, as the metric rose to a five-month high of 1.78 mn units/year. The market is forecast to struggle in the next two months however, as global oil prices spike amid the ongoing middle east conflict. South America Brazilian Light Vehicle sales totaled 177k units in February, up by 2.0% YoY. The selling rate accelerated to 2.82 mn units/year in February, up from 2.16 mn units/year in January. However, selling rates at this time of year can be distorted by the timing of Carnival, which fell in February this year, having occurred in March in 2025. Given that dealerships are often closed during the holidays, last month’s result appears impressive, as the market continues to benefit from Chinese models and electrification. In Argentina, sales totaled just under 40.0k units in February, down by 4.9% YoY. The selling rate accelerated to 555k units/year in February, from 489k units/year in January. The Argentinian auto industry is currently in a state of upheaval as there is an ongoing dispute between the government and the organizations that report vehicle sales data. However, the total sales volumes for February are believed to be accurate. "Global light vehicle market falters in February" was originally created and published by Just Auto, a GlobalData owned brand. The information on this site has been included in good faith for general informational purposes only. It is not intended to amount to advice on which you should rely, and we give no representation, warranty or guarantee, whether express or implied as to its accuracy or completeness. You must obtain professional or specialist advice before taking, or refraining from, any action on the basis of the content on our site.